The cost of a college education in the United States is rising. According to the College Board, it can cost your family $23,890 to send your student to an in-state public school, and $32,410 for a private school. To help American families with college costs, federal and state governments and colleges give more than $200 billion annually in financial aid. Your student can apply for financial aid to receive support to help meet the costs of obtaining a college education.

What is Financial Aid?

There are two types of financial aid: merit-based and need-based.

- Merit-Based scholarships are for students who have outstanding academic achievements, as well as unique talents, leadership potential, and other personal characteristics. Students may win scholarships because of group affiliation (such as YMCA, Boys Club, etc.). Students can also receive merit scholarships, awarded without regard for the financial need of the applicant. Many colleges automatically consider admitted students for merit scholarships. At other schools, however, a separate application process is required.

- Need-based financial aid is awarded based on the financial need of the student. Colleges and universities generally use the FAFSA or Free Application for Federal Student Aid for determining federal, state, and institutional need-based aid eligibility. At private institutions, a supplemental application may be necessary for need-based institutional aid.

Most often, schools will award financial aid to your student in the form of different types of funding available. These include grants, scholarships, loans, and work-study.

- Grants are federal or state free money that your student does not have to pay back.

- Scholarships are gift assistance that your student does not have to pay back.

- Loans are money that your student will borrow, either federal or private, that they will have to pay back with interest. Federal loans have income-based repayment plans, and loan forgiveness programs that provide loan relief if your student meets certain conditions.

- Work-Study is aid that your student will earn by working a part-time job while attending college.

The combination of financial aid offered depends on the availability of funds, the timeliness with which the financial aid application process is completed, and your student’s eligibility and year in school.

Your student’s financial aid package will arrive either the same day they hear back an admitted decision. Some times, the award letter will arrive 7-10 days later. Once the financial aid award letter arrives, sit down with your student to discuss if the college is affordable. If it is not, then look for instructions on how to appeal the award letter. This process may be as simple as writing a letter and providing additional documentation as requested. If you appeal and the school is still beyond your reach, you can decline the offer, citing financial difficulty (usually an OK deal breaker if you applied Early Decision), and choose another school that’s more affordable. I don’t believe any school is worth taking on tons of debt.

If you start planning now, you can secure college financial aid for your student to lessen the financial burden of a college education. Like many of my clients, I want to help you save as much as 50% off of college tuition costs.

However, you must avoid the 7 mistakes I discuss below to maximize every financial aid dollar for your student.

Mistake #1: Deciding not to apply for financial aid.

Many middle-class parents assume they make too much money and will not qualify for financial aid. But having financial need does not always mean being low-income. In college admissions, this is especially true. Many families with incomes up to $175,000 per year are eligible for some form of college financial aid.

Your family’s financial need is calculated by the FAFSA, the Free Application for Federal Student Aid. The FAFSA is a form that can be filled out annually by current and incoming college students. FAFSA will determine your student’s eligibility for federal student financial aid (including Pell grants, Stafford loans, PLUS loans, and work-study programs).

Every student should file the FAFSA every year, regardless of family income. Even if you think your student will not get need-based financial aid, many colleges will require the FAFSA for merit-based aid. If your child is a desirable candidate, the college financial aid office will make sure that finances do not prevent them from attending.

All colleges that award federal student financial aid require the FAFSA form. In addition to the FAFSA, select private colleges will also require you to complete the College Board’s CSS/Financial Aid PROFILE. Some states, such as New York where I am based, will require families to complete the New York State Tuition Assistance Program (TAP) form.

You can check school financial aid office websites for requirements for when you apply for financial aid. Many colleges have financial aid deadlines, while others have limited funding. Your family should submit the FAFSA as soon as possible after October 1 of each year.

Mistake #2: Not leveraging private scholarships.

Not applying for private scholarships can be costly. Last year, over 1.7 million private scholarships were awarded to students, accounting for $7.4 billion in financial aid. Private scholarships are offered by companies or organizations in amounts ranging from $500 to as much of the full cost of college tuition. Scholarship dollars are extra money to pay for college. Private scholarships can replace need-based financial aid awarded by colleges since it boosts resources available to the student. Scholarships should not replace merit scholarships awarded by the college since this is based on academic achievement, not finances. While applying for scholarships can be time-consuming to start, over time, a strong scholarship strategy will give you more funds to show colleges you have skin in the game.

Mistake #3: Not choosing the right colleges.

College admissions are crowded and competitive. Every year, millions of students apply to 4,000 colleges in the United States. More than 80% of American colleges accept half of their applicants. Colleges depend on students to help them decide who to admit. But also, fit and the college wanting your student to enroll in their institution impacts financial aid. Colleges often favor accepted students who have the highest GPAs and standardized test scores, rewarding them with scholarships and grants and fewer loans. Also, students who would bring diversity, culturally, socially, or economically, to the campus may be highly favored and provided with aid to minimize financial barriers to attending. For example, I had a student who received nearly full funding from Johns Hopkins because of his swimming talents.

Mistake #4: You think you can’t afford private schools.

Private schools can cost more than public schools, but private schools often have more financial aid to give. With the exception of a handful of prestigious public universities (e.g. Texas A&M, University of Michigan), generally, public schools have limited private funds, also known as endowments. And with a larger student body, public colleges and universities have to cast the financial assistance net wider. Private schools, on the other hand, often have larger endowments.

Endowments are money or financial assets that donors give to universities or colleges for investment and growth of additional income to fund future investments and expenditures. In an endowment survey conducted by InsideHigherEd to account for assets totaling $203.8 billion, public schools held 33.2 percent. Private colleges held the majority at 66.8 percent. With a larger class to provide financial aid, public colleges often cannot compete with private colleges. This makes private schools a viable option for optimal funding. Though not all private schools are created equal, search for schools that have larger endowments. It is not uncommon for families to pay more for an in-state public college than a well-endowed private college.

Mistake #5: Letting anyone other than you or your student own the 529 college savings plan.

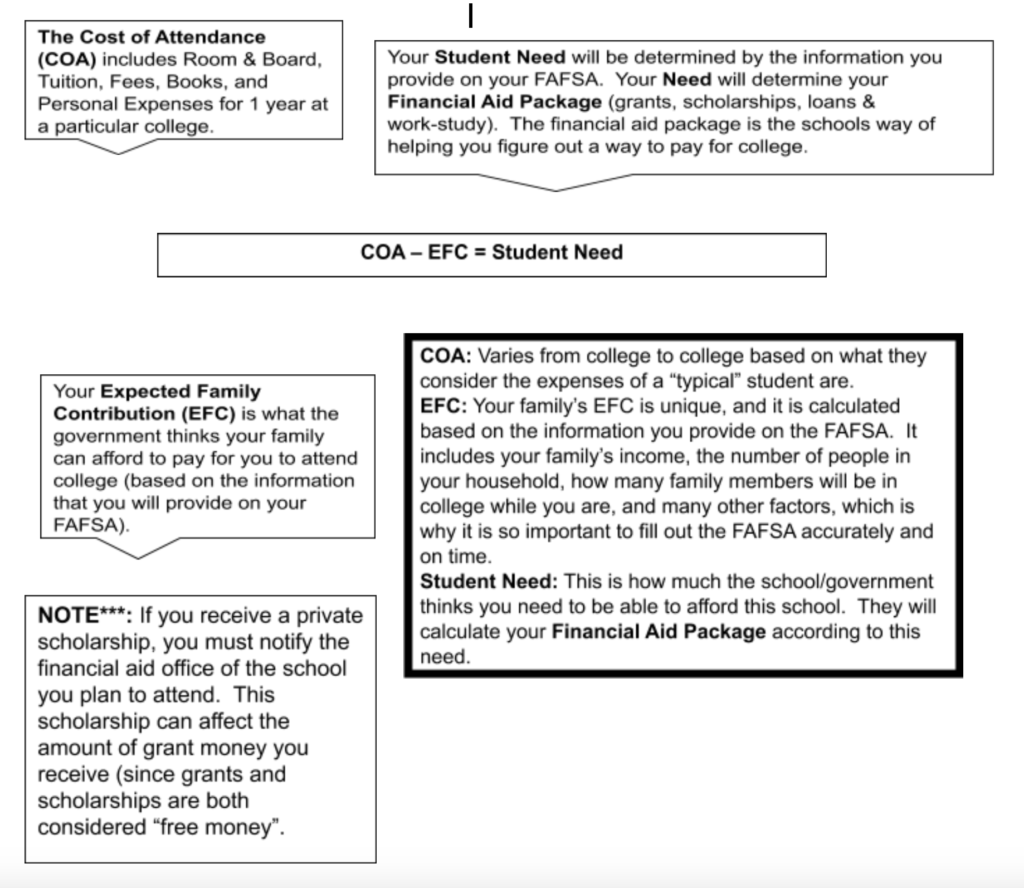

After you apply for financial aid using the FAFSA form, you will learn your Expected Family Contribution (EFC). The EFC is the amount the U.S. Department of Education believes you can pay for college expenses. When calculating EFC, FAFSA weighs assets held in the student’s name much more heavily than those in the parent’s name. And distributions taken from assets held by any other person weigh even more. Let’s take the case of the 529 college savings plan. How the 529 plan impacts the financial aid package depends on who owns it.

If the student or parent owns the 529 plan, it has minimal impact on the financial aid award. But if another family member (e.g., uncle, grandparent, cousin, etc.) own the 529 plan, the impact on financial aid eligibility can be devastating.

To illustrate the impact on the FAFSA– If reported as a parent asset, financial aid eligibility is decreased by 5.64% of the asset’s value. If reported as a student asset, financial aid eligibility is reduced by 20% of the asset’s worth, if the student has no dependents, and 3.29% if the student has dependents. If reported as a distribution from a 529 plan owned by a person other than the student or parent, financial aid eligibility is reduced by a whopping 50% of the distribution amount.

Not knowing where to keep college savings money can cost you thousands in financial aid dollars. Position college savings money strategically to maximize your financial aid.

Mistake #6: Going through the financial aid process alone to save money.

When you apply for financial aid, the process is complicated. Forms take hours to complete and require tons of documents. It can be costly if you make mistakes by way of lost financial aid dollars for your student. Mistakes can be expensive in the form of lost financial aid dollars. Consider hiring a financial aid expert who can help you navigate through the process of financial aid. On average, I have helped families applying to private schools obtain $30k to $60k in financial aid funding. With this type of financial assistance, the cost of hiring an expert pays for itself.

Mistake #7: Failing to appeal for more financial aid.

After you apply for financial aid and a college admits your student, the office of financial aid will issue an award letter. The award letter consists of forms of financial aid provided minus the cost of attendance (tuition, room and board, fees). If the amount of assistance offered is not enough, consider appealing the award decision.

Before you start the financial aid negotiation process, check with the college’s policy. Some schools have a formal process on how they handle financial aid re-evaluations. But the simplest and most used method is writing and sending a letter to your student’s assigned financial aid officer. In the letter, explain life circumstances that would make it difficult to pay for college. Examples include medical procedures, unemployment, death, or disability.

Also, explain why your student is deserving of more financial aid. Highly qualified students will undoubtedly have some leverage. Things to highlight are financial assistance offered by competing colleges, specific increase needed to make cost affordable, and documentation to support economic hardship.

I have written an article on how to negotiate a financial aid award letter that goes into the specifics of winning letters. Also, you can download a sample financial aid negotiation letter.

Conclusion

Colleges and universities have billions of dollars in financial aid that can help with college costs. Follow the advice discussed above to ensure that your student gets the money they need to pay for a college education. Lastly, there are a few other things you can do to maximize financial aid. These include:

- Applying as soon as you can after October 1.

- Making sure all personal and financial information reported is accurate.

- Reporting the correct marital information for yourself and your student.

- Not reporting stepparent’s income and assets.

- Not including stepchildren or live-in extended family in household size.

- Not explaining unusual circumstances that impact household finances.